The Struggle of 2025’s Housing Market: Rates, Builders & Buyer Squeeze

By ZoomLoans – Fast Real Estate Loans

In recent coverage, NPR (and other outlets) have painted a clear picture: the U.S. housing market in 2025 is under serious stress. Home prices are hitting record highs, yet sales are stalling. Builders are pulling back, and many potential buyers simply can’t make the math work with today’s mortgage rates. Ideastream Public Media

This isn’t just a cyclical wobble — it’s a market stuck between competing forces: ultra-tight supply, elevated borrowing costs, and homeowner “lock-in” (where current homeowners don’t want to trade up, because they’d lose their low mortgage rate).

In this post, we’ll:

- Lay out the current state of the market

- Explain how elevated mortgage rates are squeezing affordability

- Explore how homebuilding responds (or fails to respond)

- Offer actionable steps for buyers and refinancers

- Show how ZoomLoans.com/blog already addresses related themes

1. Market Snapshot: Prices Up, Sales Down, Supply Tight

- The national median sales price for existing homes has breached new highs, even while transaction volumes contract. NCPR

- Many markets now show more homes for sale than a year ago — which should help buyers — but not when mortgage costs remain so burdensome. WQLN

- New home construction is also under pressure: permits have dropped to multi-year lows, and builder incentives (price cuts, concessions) are increasingly common. WBHM

These dynamics reflect a housing market in “stasis” rather than boom or collapse. Realtor

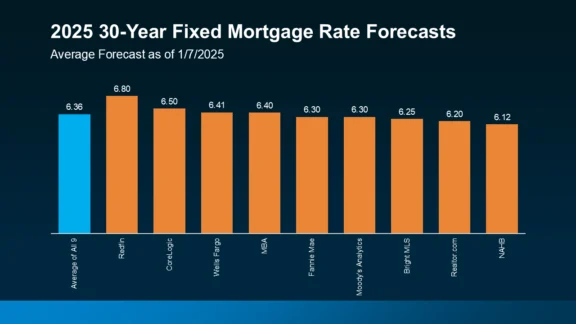

2. Mortgage Rates & Affordability: The Hidden Barrier

One of the biggest constraints right now is elevated mortgage rates. While economists hoped that recent monetary easing or rate cuts would filter into home loan costs, the drag is persistent.

- Rates around 6.7 % (or higher) are common, which adds hundreds of dollars to monthly payments compared to a few years ago. WBHM

- Even small rate cuts may be priced in ahead of time, muting their impact when they are announced. WQLN

- The “lock-in effect” is very real: homeowners with low rates are reluctant to sell, reducing turnover and keeping supply constrained. Ideastream Public Media

So what should a buyer do? Don’t wait indefinitely for “ideal” rates — perform scenario planning, get preapproved, and watch for windows to lock in favorable terms.

3. Builders & Supply: Why We Can’t Just Build Our Way Out

You might think the cure is more new homes, but that’s easier said than done in this environment:

- With high rates for construction loans and materials, building new housing is more expensive, squeezing builder margins. WBHM

- Some builders are cutting prices or offering incentives to move inventory. WBHM

- However, much of the housing shortage is a “lock-in” problem: existing owners aren’t moving, so homes never hit the market. JPMorgan Chase

Until interest rates ease meaningfully (or other structural reforms intervene), supply-side relief will remain limited.

4. What Buyers & Refinancers Can Do Now

Given these constraints, here’s how you can navigate:

- Run rate scenario analyses — use tools to see how small rate differences change affordability

- Get pre-approved now so you’re ready when rate windows open

- Watch target rate cut signals (Fed minutes, inflation data, Treasury yields)

- Consider adjustable or hybrid mortgages if you have conviction rates will drop

- Compare break-even refinancing timelines — only refinance if savings outweigh costs

5. ZoomLoans Blog Features That Help You Stay Ahead

While exploring today’s shifting housing landscape, these ZoomLoans blog posts might already be helpful:

- How the Fed Rate Cut Impacts Mortgage Rates — for deeper context on monetary policy impacts

- Fixed vs Adjustable Mortgage: What It Means in a High-Rate Market — helps you choose wisely

- When Does Refinancing Make Sense? — covers break-even, closing costs, and timing

✅ Final Thoughts

2025’s housing market is less about volatility and more about imbalance. High mortgage rates and locked-in homeowners are suppressing movement. Builders are cautious. Buyers are squeezed.

TThe path forward is incremental — not dramatic. Every percentage point you can shave off your mortgage rate, every day you save on closing costs, and every strategic move you make in timing can compound over time. Use your tools, stay informed, and link your actions to market signals.

💼 Why Work With ZoomLoans?

At ZoomLoans, we:

- Estimate your total closing costs upfront

- Help you compare loan options

- Apply for local assistance programs

- Simplify the homebuying process

🏁 Get started here: Apply for a loan today

🔗 Related Resources:

- Florida Mortgage Rates 2025

- Miami Real Estate Market for First-Time Buyers

- What to Expect on Closing Day

📞 Need Help Budgeting for Closing Costs?

Call us at (888) ZOOM-LOANS or schedule your free consultation